Using Leverage (Bank Loans) to Build a Japanese Rental Portfolio

The ability to borrow money at 2% interest and invest it at 7-10% yield is the fundamental engine of wealth creation in real estate. Japan’s historically low interest rates have made this leverage calculation unusually favorable for years. Understanding how to use bank leverage intelligentlyu2014and where the traps areu2014is essential knowledge for any serious investor.

How Japanese Bank Lending Works for Investment Properties

ud83duded2 RECOMMENDED ON AMAZON US

Real Estate Investment Books

The books that changed how I think about money, leverage, and long-term wealth.

Getting a loan for an investment property in Japan is more challenging than getting one for your own home. Banks view investment properties as higher risk, and their terms reflect that:

- Higher down payment requirement: While owner-occupied loans may allow 90-95% financing, investment properties typically require 20-30% down.

- Income scrutiny: Lenders examine your day-job income carefully. Rental income from the target property is usually not counted (or only partially counted) in your debt service ratio calculation.

- Property condition and age limits: Many banks won’t lend on pre-1981 buildings (pre-seismic standard) without seismic reinforcement work. Some set a maximum building age of 30-40 years.

- Loan-to-value (LTV) caps: Based on the bank’s appraised value of the property, not the purchase price. If you’re buying a bargain below appraised value, this can work in your favor. If you’re overpaying, you may face a financing gap.

The types of lenders I’ve worked with, in order of accessibility for individual investors:

- Regional banks (u5730u65b9u9280u884c)u2014most flexible on older properties and smaller investors

- Shinkin banks (u4fe1u7528u91d1u5eab)u2014excellent for established local investors

- Mega banks (u30e1u30acu30d0u30f3u30af)u2014strict criteria, better rates if you qualify

- Non-bank lenders (u30ceu30f3u30d0u30f3u30af)u2014higher rates but more flexible on property type and age

The Leverage Math: How Returns Are Amplified

ud83duded2 RECOMMENDED ON AMAZON US

Financial Calculators for Investors

Run yield and cash-flow calculations in seconds u2014 worth every yen on your first deal.

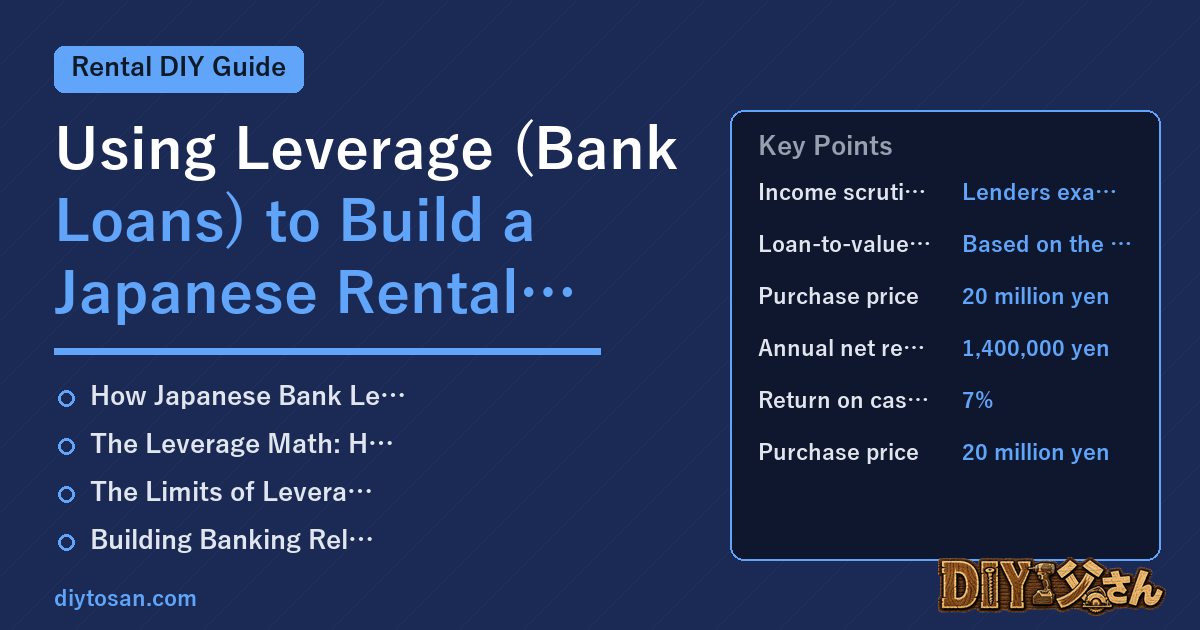

A concrete example illustrates why leverage is so powerful:

Scenario A: All Cash Purchase

- Purchase price: 20 million yen

- Annual net rental income: 1,400,000 yen

- Return on cash invested: 7%

Scenario B: Leveraged Purchase

- Purchase price: 20 million yen

- Down payment (25%): 5 million yen

- Loan: 15 million yen at 2.0%, 25 years

- Annual debt service: 762,000 yen

- Annual net rental income: 1,400,000 yen

- Cash flow after debt service: 638,000 yen

- Return on cash invested (5 million yen): 12.8%

Leverage nearly doubles the cash-on-cash return. And simultaneously, the tenant is paying down your loan principal, building your equity without additional out-of-pocket investment.

The Limits of Leverage: When It Works Against You

Leverage amplifies both gains and losses. If your rental income dropsu2014due to vacancy, rent reduction, or unexpected expensesu2014while your debt service obligation remains fixed, leverage becomes a liability.

Three scenarios where overleveraged investors get into serious trouble:

- Rising interest rates: Variable-rate borrowers who bought at 1.5% face pain if rates rise to 3-4%. On a 30 million yen portfolio, that’s an additional 450,000-750,000 yen in annual interest costs.

- Extended vacancy: A building that sits 50% vacant for 6 months while debt service continues can exhaust an under-capitalized investor’s reserves quickly.

- Catastrophic repair: An unexpected 2 million yen roof replacement with no reserves and tight cash flow can force a distressed sale.

My personal leverage rules: I maintain a minimum DSCR (net operating income u00f7 annual debt service) of 1.3 across my portfolio. I keep cash reserves equal to 6 months of total debt service. And I always stress-test a purchase at an interest rate 1.5% higher than my actual rate before committing.

Building Banking Relationships That Support Portfolio Growth

ud83duded2 RECOMMENDED PRODUCTS

Investment Analysis Templates

Spreadsheet analysis is the difference between a good deal and a disaster.

As your portfolio grows, your banking relationships become a strategic asset. I’ve cultivated three bank relationships over the years, and each handles different parts of my portfolio based on their lending criteria and rates.

What makes a good banking relationship in Japan:

- Meet with your relationship manager (u62c5u5f53u8005) at least twice a year, even when you’re not borrowing

- Always pay on timeu2014your payment history is your most valuable credential

- Share your financial statements proactively; transparency builds trust

- When your banker changes positions (which happens frequently at Japanese banks), quickly establish a relationship with their replacement

The bank that financed my first property is now a reliable partner for my third and fourth. The relationship took years to build, but it gives me a significant competitive advantage when a good property becomes available and I need to move quickly.

Property Cash Flow Calculator + Complete Guide

The exact Excel spreadsheet I use for every property purchase decision u2014 5-year projection, yield calculation, and break-even analysis included.

ud83cudfe0 More from DIY Father

15 years of landlord experience u00b7 3 apartment buildings u00b7 DIY renovations that saved millions of yen. Browse all articles at diytosan.com