Calculating ROI on Japanese Rental Property: The Real Numbers

When I was shopping for my second property, I noticed that most listings advertised a “surface yield” (u8868u9762u5229u56deu308a) that looked attractiveu2014sometimes 8%, 10%, even 12%. What they don’t tell you is that the real cash return, after you account for vacancies, repairs, taxes, and loan costs, is often half that. Let me show you how to calculate actual ROI so you don’t get fooled by headline numbers.

Surface Yield vs. Net Yield: Understanding the Difference

ud83duded2 RECOMMENDED ON AMAZON US

Real Estate Investment Books

The books that changed how I think about money, leverage, and long-term wealth.

Surface yield (u8868u9762u5229u56deu308a) is the number you’ll see on every listing site in Japan. The formula is simple:

Surface Yield = Annual Gross Rent / Purchase Price u00d7 100

Example: A property priced at 10 million yen with four units renting at 50,000 yen each generates 2.4 million yen per year. Surface yield = 24%. Sounds amazing, right? But this number assumes 100% occupancy and zero expenses.

Net yield (u5b9fu8ceau5229u56deu308a) is what actually matters. The formula:

Net Yield = (Annual Gross Rent u2212 Annual Expenses) / (Purchase Price + Acquisition Costs) u00d7 100

Using the same property, let’s work through realistic numbers:

- Annual gross rent at 90% occupancy: 2,160,000 yen

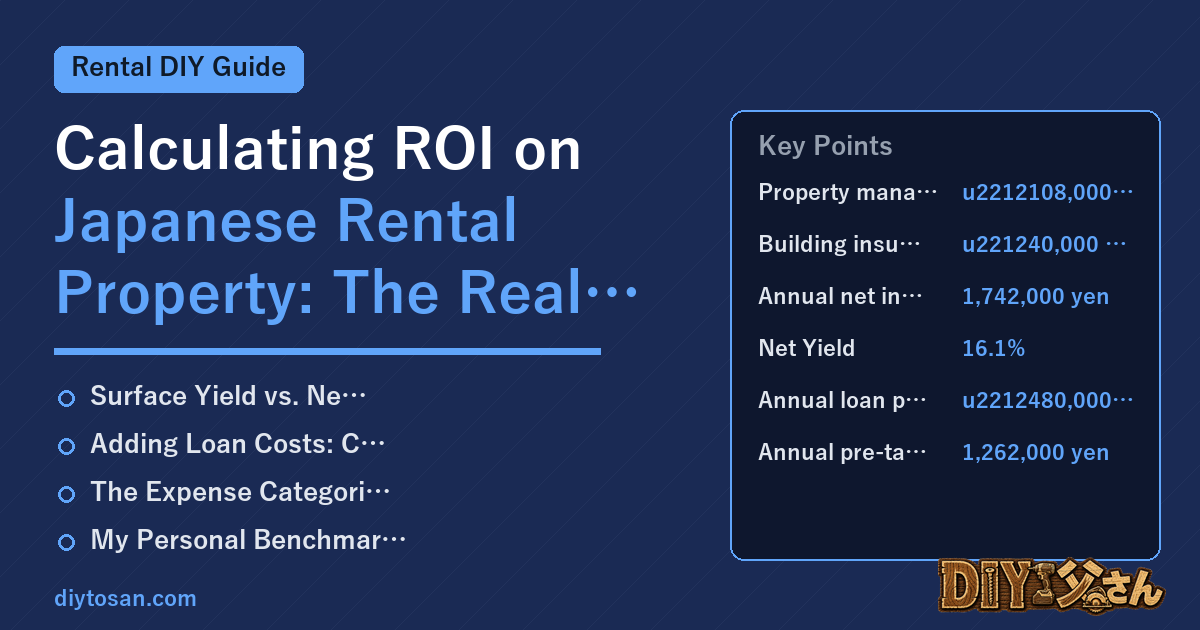

- Property management fee (5%): u2212108,000 yen

- Fixed asset tax (u56fau5b9au8cc7u7523u7a0e): u2212120,000 yen

- Building insurance: u221240,000 yen

- Repair and maintenance reserve: u2212150,000 yen

- Annual net income: 1,742,000 yen

- Total acquisition cost (purchase + 8% fees): 10,800,000 yen

- Net Yield: 16.1%

That’s still goodu2014but I chose a simplified example. In many urban markets, properties listed at 8% surface yield often deliver 4-5% net yield once everything is counted.

Adding Loan Costs: Cash-on-Cash Return

ud83duded2 RECOMMENDED ON AMAZON US

Financial Calculators for Investors

Run yield and cash-flow calculations in seconds u2014 worth every yen on your first deal.

If you’re financing the purchase (and most investors are), you need to calculate cash-on-cash returnu2014what you actually pocket relative to the cash you put in.

Let’s say I bought the above property with 3 million yen down and a 7.8 million yen loan at 2.2% interest over 20 years. Monthly payment: approximately 40,000 yen, or 480,000 yen per year.

- Annual net income before debt: 1,742,000 yen

- Annual loan payments: u2212480,000 yen

- Annual pre-tax cash flow: 1,262,000 yen

- Cash invested (down payment + acquisition costs): 3,800,000 yen

- Cash-on-Cash Return: 33.2%

This looks fantastic, but I haven’t accounted for income tax on the rental profits. Depending on your tax bracket and whether you can offset income with depreciation (more on that in another article), your after-tax return will be lower.

The Expense Categories You Must Track

After managing properties for over a decade, here are the expense categories I track religiously:

- Vacancy loss: In my experience, budget 8-10% annually. Even good properties have turnover.

- Property management: If you self-manage like I do, the cost is your time. If you hire a management company, expect 5-8% of collected rent.

- Fixed asset tax (u56fau5b9au8cc7u7523u7a0e + u90fdu5e02u8a08u753bu7a0e): Typically 1.4% + 0.3% of assessed value per year. For older properties, assessed value is often well below purchase price.

- Building insurance: Fire and earthquake insurance. Factor 30,000-80,000 yen per year depending on building size and type.

- Repairs and capital expenditures: Budget 1-2% of building value per year for ongoing maintenance, and maintain a separate reserve for major items (roof, water heater, exterior painting).

- Advertising and tenant-finding fees: Typically 1 month’s rent paid to the leasing agent per new tenant. With a 2-year average tenancy, this equals about half a month’s rent annually per unit.

My Personal Benchmark Numbers

ud83duded2 RECOMMENDED PRODUCTS

Investment Analysis Templates

Spreadsheet analysis is the difference between a good deal and a disaster.

After years of doing this, here’s what I look for before buying:

- Surface yield: at least 8% in regional cities, 6% in major cities

- Net yield: at least 5% after all operating expenses

- Positive cash flow even in a scenario with 85% occupancy

- Debt service coverage ratio (DSCR) above 1.3 (net income is at least 1.3x annual loan payments)

If a property doesn’t meet these thresholds on paper, I walk away. There are always other deals. The discipline to say no to mediocre investments is what separates investors who build wealth from those who break even.

Property Cash Flow Calculator + Complete Guide

The exact Excel spreadsheet I use for every property purchase decision u2014 5-year projection, yield calculation, and break-even analysis included.

ud83cudfe0 More from DIY Father

15 years of landlord experience u00b7 3 apartment buildings u00b7 DIY renovations that saved millions of yen. Browse all articles at diytosan.com