How Depreciation Calculation Works for Rental Property in Japan

Depreciation is the most powerful u2014 and most misunderstood u2014 tax tool available to Japanese landlords. When I first bought my rental property, I thought depreciation was something complicated that only accountants could calculate. In reality, the mechanics are straightforward once you understand the system. Getting this right can save you hundreds of thousands of yen in taxes each year.

What Depreciation Actually Is

ud83duded2 RECOMMENDED ON AMAZON US

Personal Finance & Real Estate Books

The financial mindset shift that made property investment possible on a salary.

Depreciation (u6e1bu4fa1u511fu5374) is the accounting recognition that buildings and fixtures wear out over time. Japan’s tax law allows you to deduct a portion of your building’s acquisition cost each year over its statutory useful life (u6cd5u5b9au8010u7528u5e74u6570), even though you are not actually spending that cash. This makes depreciation a non-cash deduction u2014 you reduce your taxable income without any additional out-of-pocket expense.

Critically, land does not depreciate. Only the building (and fixtures within it) qualifies. When you purchase a property, you must separate the purchase price into land value and building value. This allocation is typically found in the sale contract, or you can use the fixed asset tax assessment (u56fau5b9au8cc7u7523u7a0eu8a55u4fa1u984d) ratio to split the purchase price.

For example: if you paid u00a525,000,000 for a property, and the fixed asset tax assessment shows land at u00a512,000,000 and building at u00a58,000,000 (a 60/40 ratio), then the building portion of your purchase price is u00a525,000,000 u00d7 40% = u00a510,000,000. This u00a510,000,000 is the depreciable base.

Statutory Useful Life by Construction Type

ud83duded2 RECOMMENDED ON AMAZON US

Budget Planners for Property Owners

Track every yen in and out u2014 the foundation of profitable landlord accounting.

Japan sets a fixed statutory useful life for each type of building construction. The most common types for residential rental property are:

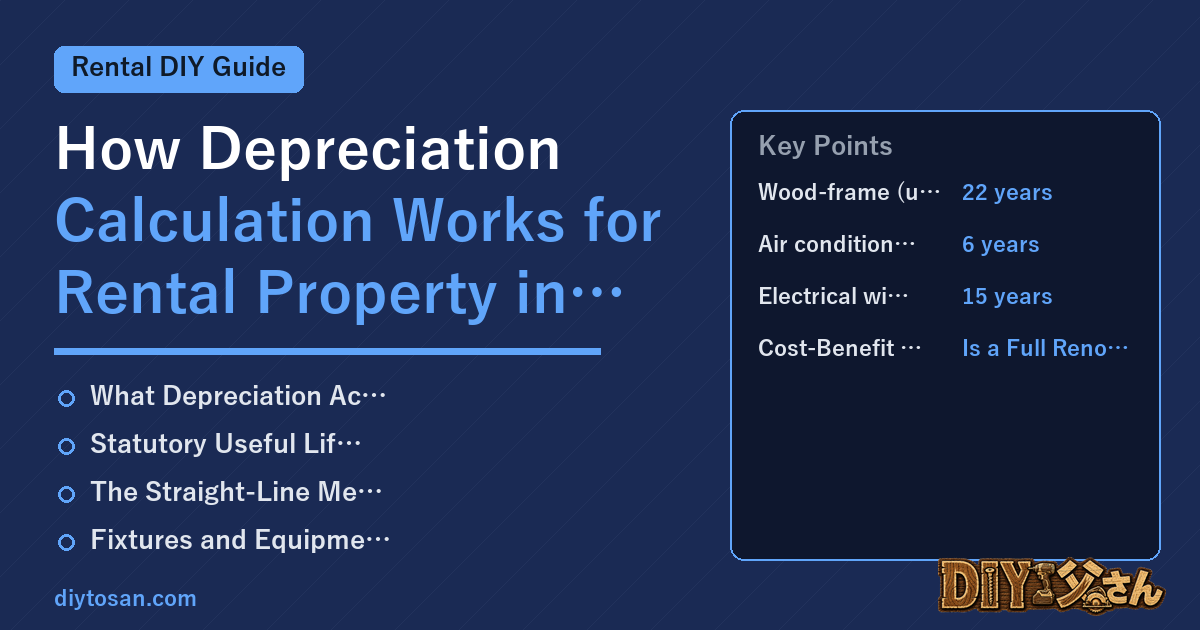

- Wood-frame (u6728u9020): 22 years

- Light steel frame, wall thickness 3mm or less (u8efdu91cfu9244u9aa8): 19 years

- Light steel frame, wall thickness 3u20134mm (u8efdu91cfu9244u9aa8): 27 years

- Heavy steel frame (u91cdu91cfu9244u9aa8): 34 years

- Reinforced concrete (RCu9020/u9244u7b4bu30b3u30f3u30afu30eau30fcu30c8): 47 years

- Steel-reinforced concrete (SRCu9020): 47 years

If you purchase a used building that is already partially depreciated, the remaining useful life is calculated differently. For a used building, the formula is: remaining life = statutory life u2212 years already elapsed + (years elapsed u00d7 0.2). If the result is less than 2 years, the remaining life is set at 2 years.

The Straight-Line Method: How to Calculate Your Annual Deduction

For buildings acquired after 2007, Japan mandates the straight-line method (u5b9au984du6cd5) for real estate. The formula is simple:

Annual depreciation = Depreciable base u00d7 Depreciation rate

The depreciation rate for each useful life is published by the NTA. Key rates: 22-year life = 0.046, 27-year life = 0.038, 34-year life = 0.030, 47-year life = 0.022.

Working through an example: You buy a used wood-frame apartment building. The building is 10 years old, so the remaining useful life is: 22 u2212 10 + (10 u00d7 0.2) = 14 years (round down). The depreciation rate for 14 years = 0.072. Your building’s depreciable base is u00a58,000,000. Annual depreciation = u00a58,000,000 u00d7 0.072 = u00a5576,000 per year.

That u00a5576,000 comes straight off your taxable rental income every year for 14 years, with no cash outlay. If you are in a combined marginal tax bracket of 30% (income tax + inhabitant tax), this depreciation saves you u00a5172,800 in taxes annually.

Fixtures and Equipment: Separate Depreciation Schedules

ud83duded2 RECOMMENDED PRODUCTS

Tax Guides for Property Investors

Knowing the tax rules turns a good investment into a great one.

Beyond the building itself, fixtures and equipment you install in rental units also depreciate on their own schedules. Common items and their statutory lives:

- Air conditioners (built-in): 6 years

- Water heaters (u7d66u6e6fu5668): 6 years

- Kitchen systems (u30b7u30b9u30c6u30e0u30adu30c3u30c1u30f3): 5 years (if separate from building)

- Bathroom fixtures (u30e6u30cbu30c3u30c8u30d0u30b9): 15 years

- Electrical wiring (added): 15 years

- Flooring (u30d5u30edu30fcu30eau30f3u30b0 as capital improvement): 15 years

Items costing less than u00a5100,000 each can generally be expensed in full in the year of purchase rather than depreciated over their useful life. For items between u00a5100,000 and u00a5300,000, a special small-business provision (u5c11u984du6e1bu4fa1u511fu5374u8cc7u7523u306eu7279u4f8b) allows full immediate expensing if you qualify as a small business u2014 but the application of this rule to individual landlords is nuanced, so verify with your tax accountant.

Depreciation is the cornerstone of rental property tax planning in Japan. Mastering these calculations u2014 or ensuring your accountant is applying them correctly u2014 is not optional if you want to manage your properties efficiently.

Renovation Cost Reduction Checklist (60% Savings Method)

My step-by-step process management template that cut renovation costs by 60% across 3 apartment buildings over 15 years.

ud83cudfe0 More from DIY Father

15 years of landlord experience u00b7 3 apartment buildings u00b7 DIY renovations that saved millions of yen. Browse all articles at diytosan.com